Surprise! Your financial aid award letter doesn’t make sense. Here’s how to measure your true cost of college.

Getting college acceptance letters is a huge relief. It’s no longer a guessing game. Once you’ve celebrated, expect another piece of the puzzle to arrive. Your financial aid award letter.

Trouble is, they’re not as straightforward as an acceptance letter. Either you’re in or not. With award letters, colleges tend to use their own vocabulary, tables with the financial aid breakdowns and leave out anything they wish.

Confused by what your award letters mean?

You’re not alone!

This lack of transparency spurred this study by New America and uAspire, a college affordability nonprofit, examining the lack of transparency in award letters. By analyzing 11,000+ letters, they found students (who were offered a Pell Grant) ended up owing significantly more than estimated. This equated to an average of nearly $12,000.

Of these 11,000 letters studied, they pulled 515 award letters for an in-depth analysis. Trends across the letters were omission of total costs, inconsistent terminology (136 unique terms for “loan”, including 24 that didn’t include the word at all), vague or no definitions, and among other findings.

How to read your award letter

Getting an answer to the true cost of college means cutting through their jargon and focusing on exactly what they’re telling you. In other words, how much money do you need to pay back and what amount is given to you for free?

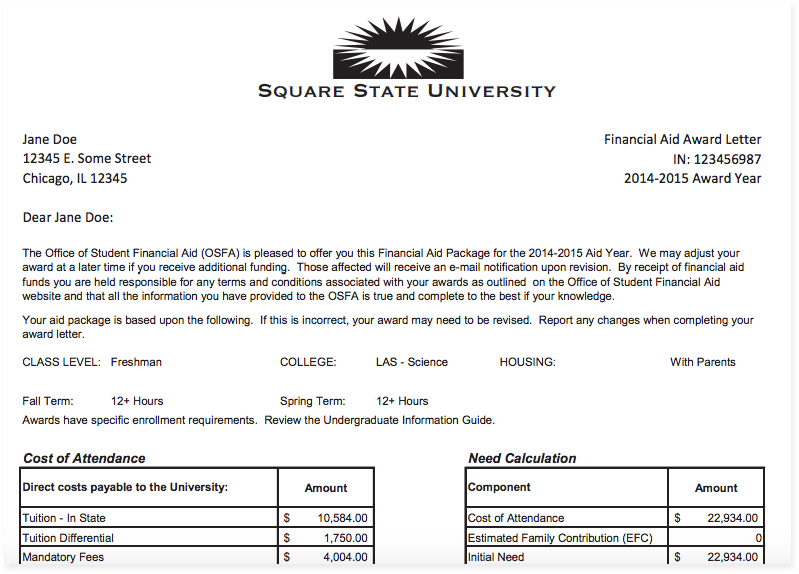

Let’s use this sample award letter as a guide:

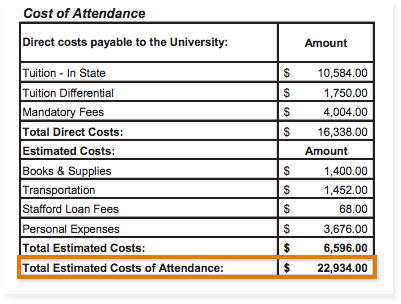

1) Calculate your Cost of Attendance (COA):

COA = Tuition and fees + on-campus room and board (or a housing and food allowance for off-campus students) + books + supplies + transportation + loan fees

Ex: Cost of Attendance = $22,934

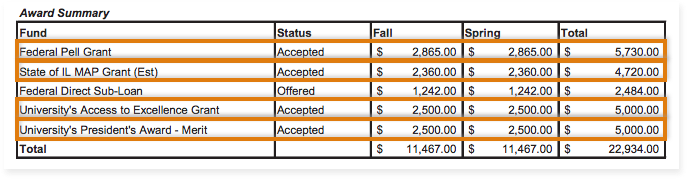

2) Subtract free money from COA:

Federal Pell Grant + scholarships + state/institutional grants + military education benefits

Ex: $20,450 (free money) – $22,934 (COA) = $2,484

3) Subtract work study money from COA:

Federal work-study + state work-study + institutional work-study

This may or may not be listed in your estimate. With our example, there’s no mention of work-study.

Ex: Work study = $0

4) Subtract loans/money you plan to borrow from COA:

Federal direct subsidized student loan + federal direct unsubsidized student loan + federal PLUS loan

Ex: Money you plan to borrow: $0 (let’s say you want to avoid taking out any loans)

Which means the totals are:

$20,450 (free money) – $22,934 (COA) – $0 (work study) – $0 (loans) =

Your out-of-pocket of attending Sample College for one year: $2,484

When comparing letters, keep these things in mind

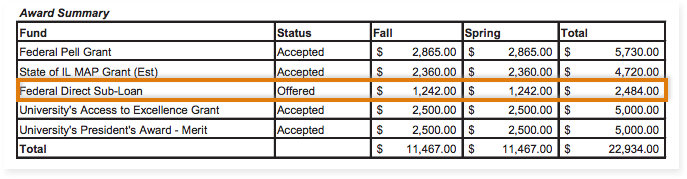

Don’t feel obligated to take out loans. They’re always optional. Notice how the sample letter automatically added the Federal Direct Subsidized Loan of $2,484 to cover your out-of-pocket cost and make it seem as though your student would attend for free.

Look out for loans lumped in with free money. In this case, the Federal Direct Subsidized Loan mixes with grants and merit aid under “Awards” and this grouping makes it look like a grant or scholarship when it’s not.

If you see “Est” next to grants and scholarships, pay particular attention, especially if you’re unsure about the amount of income on your FAFSA/CSS Profile. Colleges base their estimates off your income and assets in 2017 for the 2019-2020 school year. Depending on any discrepancies, your out-of-pocket cost can vary by hundreds or even thousands of dollars.

Be careful about words they choose to leave out, too.. You may notice “Parent PLUS” listed as an award. It’s not free money. It’s a loan that needs to be repaid with interest.

If you’re unsure about what exactly they’re saying you owe and your award offerings, consult a financial aid expert for help. Remember: Although difficult questions and potentially expensive pitfalls are inevitable in the college planning process, you’re not alone!

Westface College Planning helps take the stress out of paying for college. If you need help navigating your college financial plan, give us call, sign up for a Tackling the Runaway Costs of College webinar or schedule a free consultation with Beatrice Schultz, CFP®.

Ready for your own success story?

If you’re a typical parent with college-bound students, you’re probably overwhelmed. You want to help your sons and daughters make the right choices and prevent overpaying for their education. You’re not alone! We’re here to help. Schedule your free consultation today – click below to get started!

Catch our free, on-demand webinar:

How to Survive Paying for College

Join Beatrice Schultz, CFP® for our on-demand webinar, where she provides parents with the exact steps that often greatly lower the cost of college, even if there’s little time to prepare.